Switching Health Plans? How Generic Drug Coverage Can Save You Hundreds Annually

When you’re switching health plans, the biggest mistake most people make? They focus only on monthly premiums and ignore what happens when they actually need to fill a prescription. If you take even one generic medication regularly - like metformin for diabetes, lisinopril for high blood pressure, or levothyroxine for thyroid issues - the difference in how your new plan covers generics could mean hundreds or even thousands in extra costs every year.

Why Generic Drug Coverage Isn’t Just a Detail

Generic drugs aren’t cheap because they’re less effective. They’re cheap because they’re the same medicine, made after the patent on the brand-name version expires. The FDA requires them to have the same active ingredients, strength, and dosage. But your insurance doesn’t always treat them that way. In 2023, generics made up 90% of all prescriptions filled in the U.S., yet they accounted for only 23% of total drug spending. That’s because they work. And when your plan covers them well, you save big. But not all plans cover them the same. Most health plans use a tiered system called a formulary. Think of it like a ladder. The lower the tier, the less you pay. Tier 1 is almost always reserved for generics. But here’s where it gets tricky: some plans charge you $3. Others charge $20. Some waive your deductible for Tier 1. Others make you pay the full deductible before you even get to Tier 1.Tier Structures You Need to Know

There are three main formulary structures you’ll run into:- 3-tier plans: Common in some employer plans. Tier 1: generics ($5-$10 copay). Tier 2: brand-name drugs. Tier 3: specialty drugs.

- 4-tier plans: The standard for marketplace plans under the Affordable Care Act. Tier 1: generics ($3-$20). Tier 2: preferred brands. Tier 3: non-preferred brands. Tier 4: specialty drugs.

- 5-tier plans: Often seen in Medicare Advantage plans. Tier 1: preferred generics ($0-$10). Tier 2: non-preferred generics ($20-$40). Tier 3-5: brands and specialties.

How Deductibles Change Everything

This is where people get burned. Many plans - especially high-deductible health plans (HDHPs) - bundle your medical and prescription deductibles. That means if your deductible is $2,000, you pay 100% of your generic drug costs until you hit that number. Even if your plan says “Tier 1 generics: $20 copay,” that only kicks in after you’ve paid $2,000 out of pocket. But here’s the secret: Silver Standardized Plan Design (SPD) plans are different. Since 2014, CMS has required these marketplace plans to waive the deductible for Tier 1 generics. So even if your deductible is $3,000, you pay just $20 for your metformin. No waiting. No surprise bills. That’s why KFF found Silver SPD plans can save low-income users up to $1,200 a year on prescriptions alone. If you’re on regular medications, avoid HDHPs unless you’re healthy. They’re great for people who rarely see a doctor. Terrible for people who need meds.Medicare Part D and the Hidden Trap

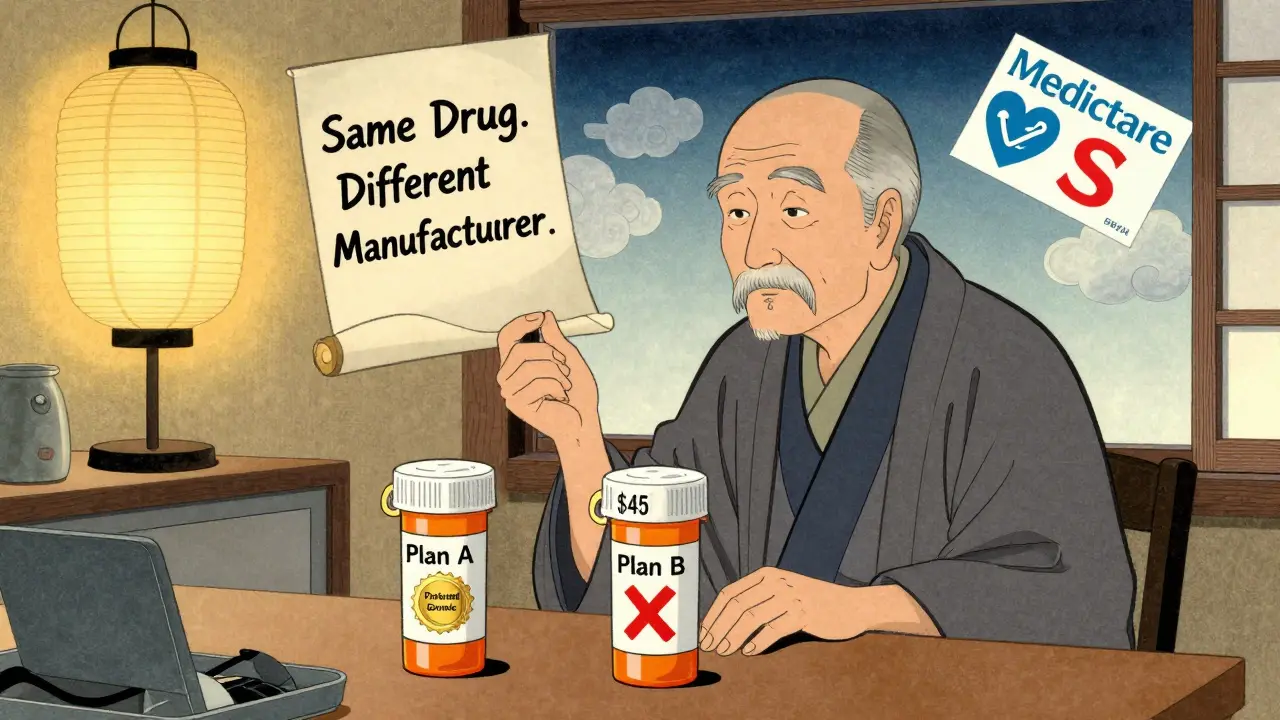

If you’re on Medicare, things get even more complicated. In 2023, the base deductible for Part D plans was $505. Most people pay that before their generic copays start. But here’s the catch: some Medicare Advantage plans (MA-PDs) have lower out-of-pocket costs than standalone Part D plans. According to Medicare’s own data, MA-PDs save users 18% on average for generic drugs. But not all generics are treated equal. Some plans label your generic as “preferred” (Tier 1). Others label it “non-preferred” (Tier 2) - even if it’s the exact same drug. One user on Medicare.gov reported paying $0 for levothyroxine under Plan A, then $45 under Plan B - same drug, same manufacturer, different plan. Why? Because plans can choose which manufacturers they prefer. If your current generic is made by Manufacturer A, and your new plan only covers Manufacturer B, you could be bumped up to a higher tier - and pay double.

State Rules Can Change Your Costs Overnight

California has a $85 outpatient drug deductible. New York waives deductibles for generics entirely. DC has a $350 separate drug deductible. These rules don’t change based on your federal plan - they’re state laws. If you move from New York to California, your $3 generic copay could suddenly become a $85 deductible plus 20% coinsurance. That’s a 5x cost increase. KFF found that states with separate drug deductibles - like California, New Jersey, and Illinois - see 22% higher medication adherence. Why? Because people don’t skip doses to save money. If your state requires you to pay the first $85, you’re more likely to budget for it. But if you’re used to $3 copays, that $85 feels like a punch.What You Must Check Before Switching

Don’t guess. Don’t assume. Don’t trust the sales rep. Here’s what you need to verify:- Your exact drug name and manufacturer: Is it “metformin ER 500mg” or “metformin 500mg”? Are you on the brand made by Teva or Mylan? Some plans cover one, not the other.

- Which tier: Is it Tier 1 or Tier 2? Ask for the full formulary, not just a summary.

- Pharmacy network: Is your local pharmacy in-network? If not, your $3 copay could jump to $120.

- Deductible integration: Does your plan combine medical and drug deductibles? If yes, you’re paying full price until you hit the total.

- Mail-order vs retail: Some plans charge less if you get a 90-day supply by mail. Others charge more.

Tools That Actually Work

Use these tools - not just to compare, but to calculate:- Medicare Plan Finder: Enter your drugs, zip code, and pharmacy. It shows real out-of-pocket costs. Over 4 million people used it in 2022.

- eHealthInsurance’s Prescription Calculator: Filters plans by your exact medications. Processes 1.7 million queries a month.

- Insurer-specific formulary tools: Blue Cross, UnitedHealthcare, Humana - all have searchable formularies on their websites. Accuracy? Up to 96%.

What’s Changing in 2025 and Beyond

The Inflation Reduction Act of 2022 capped insulin at $35/month - and it’s now law. Starting in 2025, Medicare Part D will cap out-of-pocket drug costs at $2,000 a year. That’s huge. But there’s a twist: Medicare is splitting generics into two tiers in 2025 - Tier 1 (preferred) and Tier 1+ (non-preferred). That means even if you’re on a generic, you might pay more if your drug isn’t on the “preferred” list. Meanwhile, more states are creating separate drug deductibles. And AI tools like CMS’s new “Medicare Plan Scout” are making it easier to compare plans - reducing enrollment errors by 44% in testing.Real Stories, Real Savings

One woman in Oregon switched from a $40/month premium plan to a Silver SPD plan with a $3 generic copay. She took three generics. Her annual drug cost dropped from $1,200 to $432. That’s $768 saved. Another man in Florida thought his new plan was cheaper because the premium was $10 lower. He didn’t check the formulary. His levothyroxine went from $0 to $25. He ended up paying $300 more that year. These aren’t edge cases. They’re common.Final Rule: Always Run the Numbers

You wouldn’t buy a car without checking the fuel efficiency. Don’t pick a health plan without checking your prescriptions. Take your list of medications. Go to the plan’s formulary. Look up each one. Note the tier. Check the pharmacy. Calculate the annual cost. Compare it to your current plan. The difference between a good plan and a bad one isn’t the premium. It’s what you pay when you walk into the pharmacy. If you take generics - and you probably do - this one step could save you more than any other decision you make this year.Are all generic drugs covered the same across health plans?

No. Even if two plans cover the same generic drug, they might place it on different tiers. One plan might list it as Tier 1 (lowest cost), while another lists it as Tier 2 (higher cost) based on which manufacturer they prefer. Always verify the exact drug name and manufacturer on the new plan’s formulary.

Do I still pay a deductible for generic drugs?

It depends. In Silver Standardized Plan Design (SPD) plans, deductibles are waived for Tier 1 generics - you pay a fixed $3-$20 copay regardless of your deductible. But in most other plans, including high-deductible health plans (HDHPs), you must meet your full medical and prescription deductible before any drug coverage kicks in. Always check whether your plan combines or separates medical and drug deductibles.

Can I switch to a cheaper plan if my generic drug is no longer covered?

Yes - but timing matters. You can only switch plans during Open Enrollment (November-December for Medicare, January-March for marketplace plans). If your drug is removed mid-year, you may qualify for a Special Enrollment Period if you lose coverage or move. Always request a formulary change request from your plan if a drug is removed - sometimes they’ll reinstate it.

Why does my generic drug cost more on a new plan even though it’s the same medicine?

Because plans choose which manufacturers they cover at the lowest tier. If your current plan covers metformin made by Teva as Tier 1, but your new plan only covers metformin made by Mylan at Tier 1, you may be moved to Tier 2 - even if the drug is chemically identical. Always check the manufacturer listed on the formulary.

Are there tools to compare generic drug costs between plans?

Yes. Medicare.gov’s Plan Finder, eHealthInsurance’s prescription calculator, and insurer-specific formulary search tools let you enter your medications and see estimated annual costs. These tools are far more accurate than relying on premium or general coverage descriptions. Users who use them save an average of 32% on prescription costs.

Andrew Poulin

March 6, 2026 AT 12:43Stop wasting time on premiums. Your meds are the real cost.

Check the formulary. Not the ad.

If your metformin jumps from $3 to $20, you just lost a grand a year.

Simple.

Sean Callahan

March 6, 2026 AT 13:42so i switched plans last year and thought i was gettin a deal til i realized my levothyroxine went from 0 to 45??

like wtf man i was on the same drug

called customer service and they said 'oh we dont cover teva anymore' lol

im still salty

and yes i know its the same chemically but why do they do this??

also my pharmacy network changed and now i gotta drive 20 mins

so much for 'convenience'

anyone else feel like insurance companies are playing 4d chess with our health??

and why is there no app that just tells you the real cost??

why do i have to dig through 3 websites??

fr

Ferdinand Aton

March 7, 2026 AT 06:30Actually, the whole 'generic = cheaper' thing is a myth.

Most people don't realize that brand-name drugs often get rebates that lower the net cost to insurers.

So sometimes, the 'expensive' brand is actually cheaper for the plan.

And that's why they push generics to Tier 2.

It's not about your savings - it's about their profit margins.

Also, Medicare Advantage plans? They're basically insurance companies in disguise.

They cherry-pick the healthiest seniors and dump the rest.

Don't trust anything you hear from a 'plan advisor'.

They get paid if you pick their plan - not if it's good for you.

And don't even get me started on mail-order.

They'll make you wait 2 weeks for your meds just to save $1.50.

It's a scam.

But hey, at least we're 'saving money'.

William Minks

March 7, 2026 AT 15:36Just wanna say THANK YOU for this post 🙏

My mom’s on 4 meds and I spent 3 days comparing plans last year.

Used Medicare Plan Finder + eHealth + Blue Cross tool.

Turns out her Tier 1 generic was Tier 2 on her old plan.

She saved $912 in Year 1.

Also, the Silver SPD waiver? Life-changing.

She didn’t even know it existed.

PS: If you’re in CA, check out CalRx - state’s pushing for $0 generics by 2026 🚀

Stay informed, folks. This stuff matters.

Jeff Mirisola

March 9, 2026 AT 15:35This is the most important thing I’ve read all year.

People think 'health insurance' means 'health care'.

Nope.

It means 'cost containment with side effects'.

I work in a clinic.

I see people skipping meds because their copay went from $3 to $45.

One guy stopped his blood pressure med because he couldn’t afford it.

Three months later, he had a stroke.

Insurance companies don’t care about outcomes.

They care about premiums and claims ratios.

So if you’re switching plans, don’t just compare premiums.

Compare your meds.

Write them down.

Call the pharmacy.

Ask for the formulary PDF.

Don’t trust a rep.

And if you can’t afford it?

Ask for a patient assistance program.

They exist.

And yes, this is a systemic failure.

But you can still win this round.

Susan Purney Mark

March 11, 2026 AT 06:43Thank you for writing this. 🤍

My sister just got diagnosed with hypothyroidism and I helped her switch plans.

We used the Medicare Plan Finder and found that Plan A charged $0 for levothyroxine - but only if she used CVS.

Plan B had a $5 copay but covered 50 pharmacies.

She picked Plan B because she doesn’t want to drive across town every month.

Also - the state deductible thing? Mind blown.

I’m in NY - we get waivers.

My cousin in NJ? Paying $350 before anything.

It’s insane how location changes your life.

And yes, manufacturer matters.

She was on Teva. New plan only covered Mylan.

They’re chemically identical - but insurance treats them like different drugs.

So dumb.

But I’m glad tools exist.

Just wish they were easier to find.

Also - if you’re on Medicaid, check out 340B pharmacies.

Game changer.

Joey Pearson

March 12, 2026 AT 08:17My dad’s on 3 generics.

Switched from a $200/month plan to a $140 one.

Thought he was saving.

His copays went from $5 to $22 each.

Annual cost: $1,080 → $2,592.

He didn’t check.

Now he’s on a Silver SPD plan.

Back to $5.

He saved $2,000.

Don’t assume.

Don’t guess.

Do the math.

It takes 20 minutes.

You’re worth it.

Roland Silber

March 13, 2026 AT 21:14Great breakdown - but let’s go deeper.

One thing no one talks about: therapeutic substitution.

Some plans don’t just move you to a higher tier - they swap your generic for a different one.

Same active ingredient? Sure.

But different inactive ingredients - binders, dyes, fillers.

For some people, that causes reactions.

My cousin had an allergic reaction to a generic switch - turned out it was a dye change.

Insurance didn’t care.

They said ‘it’s the same drug’.

But biologically? Not always.

Also - formularies change monthly.

Just because it’s Tier 1 today doesn’t mean it will be next month.

Set a calendar reminder.

Check your plan every 90 days.

And if you’re on Medicare, use the ‘plan change request’ form.

They’re required to respond within 72 hours.

Knowledge is power - but consistent vigilance? That’s survival.